5

5

03

01

December is a strange time for money.

You’re wrapping up the year…

You’re reflecting on what worked and what didn’t…

And maybe — just maybe — you’re realizing things didn’t move forward as much as you hoped.

Here’s the good news:

It’s not too late to course-correct.

In fact, how you finish the year could be the biggest factor in how you start the next one.

And there’s one strategy that quietly helps people finish stronger — while creating unstoppable momentum for what’s ahead:

It’s called the Infinite Banking Concept.

For most people, December looks like this:

They wait until January to “get serious”…

Then life happens, and nothing sticks.

But momentum isn’t built on dates.

It’s built on decisions.

The Infinite Banking Concept, introduced by R. Nelson Nash, is about building a personal financial system that gives you control, flexibility, and growth — no matter what time of year it is.

It starts with a properly structured whole life insurance policy from a mutual company.

And when used the right way, it helps you:

This isn’t a flashy year-end hack.

It’s a long-term system that works year after year — with more power the longer you use it.

Imagine this:

Instead of scrambling to spend down accounts or max out random tax shelters, you end the year by:

You’re not reacting anymore — you’re strategically redirecting your money.

And that kind of clarity at the end of the year?

It sets you up to win from day one of the next.

You don’t need to wait for January 1st to start building momentum.

You can start right now — even with something small.

What matters is building a system that:

That’s the power of Infinite Banking.

It’s fine to look back.

But what matters most is what you do next.

Because momentum doesn’t come from wishing.

It comes from building a foundation that works every single day — not just when the calendar flips.

🔘 Download the Free Guide to Infinite Banking

🔘 Schedule a Call and explore how to make this your most strategic year yet

Let’s make this the year you stopped hoping — and started building.

You may have seen the recent news about NASCAR champion Kyle Busch and his wife, Samantha, claiming they lost $8.5 million inside an Indexed Universal Life (IUL) policy strategy. When something like this hits headlines, it spreads fast and it can leave people wondering whether IULs are “good,” “bad,” or something to avoid altogether.

Before jumping to conclusions, it’s important to understand what actually happened because the problem wasn’t simply that the policy was an IUL. The core issue appears to be how the policy was designed, illustrated, and communicated.

I work with families and business owners to help them control the banking function in their own lives, which is the heart of the Infinite Banking Concept. True Infinite Banking requires:

This is why the Nelson Nash Institute teaches that Infinite Banking is best implemented using dividend-paying whole life insurance from a mutual company because it provides control and certainty.

Now, yes, you can take policy loans and repay them inside an IUL. It can grow. It has cash value.

But because IULs are tied to market index performance and cost-of-insurance adjustments, you cannot fully control the banking function the same way you can with properly structured whole life.

This distinction becomes very important in the Busch situation.

According to the lawsuit, the Busches were told:

However, the complaint states that the policy:

To quote an industry attorney reviewing the case:

“If the allegations are true, this policy is a case study in how not to design and sell an IUL.”

Not necessarily.

The better answer is: It depends on the purpose and the design.

But we should not lump all “life insurance” into one bucket.

There are major structural differences:

| Whole Life | IUL / UL / VUL |

|---|---|

| Guaranteed, contractual growth | Performance tied to indexes or investments |

| Premium and cost structure is fixed and predictable | Costs can rise over time |

| Designed for stability and control | Designed around market movement and variability |

| Ideal for Infinite Banking | Not built to support banking control long term |

They are not interchangeable tools.

When whole life is designed for maximum cash value, minimal necessary death benefit, and long-term flexibility, you don’t run into the same deterioration risks that are common in IUL over time.

In my personal experience reviewing policies from new clients over the years:

Less than 10% of the IUL policies I’ve reviewed were on track to sustain themselves long term. The majority showed increasing internal charges that eventually caused the policy to collapse unless the owner injected more premiums later.

This is the opposite of control.

Which is why whole life is the foundation of Infinite Banking – not because it’s “better” emotionally, but because it is more stable structurally.

When you are trying to control the banking function, stability matters more than hypothetical upside.

This situation is your cue to review what you actually own:

If you want to know exactly how your policy works, or whether it aligns with your goals, I’m here to help.

A 30-minute conversation can prevent years of unwanted surprises.

-Jason K. Powers

-1024 Wealth

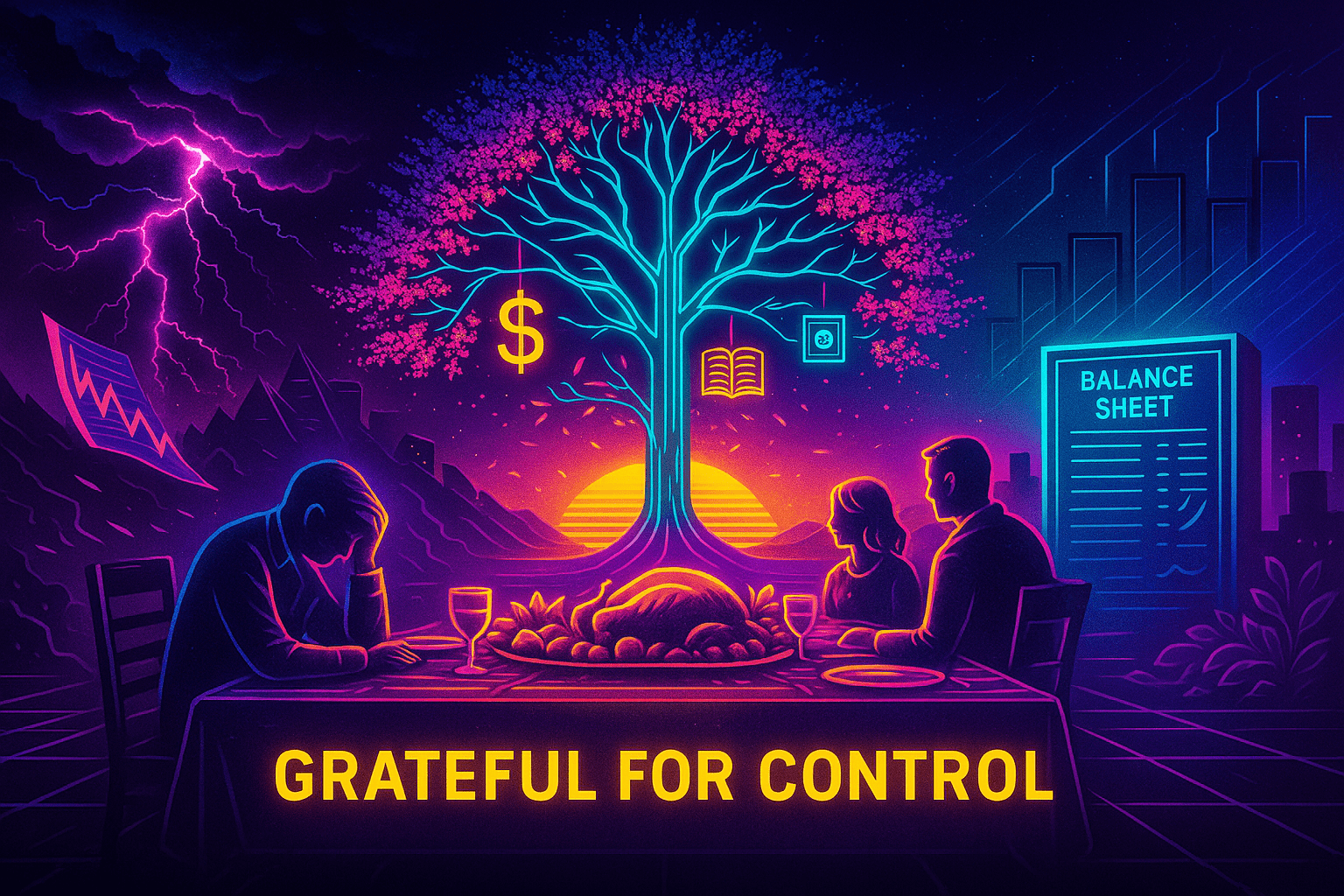

In November, we pause to give thanks.

We gather around the table.

We think about family.

We reflect on what really matters.

But here’s something few people are ever taught to be thankful for:

👉 Control over their financial life.

Because let’s be honest — most people don’t have it.

They’re stuck reacting to bills, markets, loans, or unexpected expenses.

They’re following financial advice that’s often outdated or generic.

And deep down, they’re wondering if they’re doing any of it right.

But when you implement the Infinite Banking Concept, something shifts.

You move from a place of uncertainty to a place of strategy.

And that kind of clarity?

It changes everything.

Traditional financial planning is built on a few core ideas:

That leaves people in a constant state of waiting, worrying, and hoping.

And it’s hard to feel gratitude when you’re not confident.

Infinite Banking, introduced by R. Nelson Nash, flips the script.

Instead of depending on external systems, you build your own.

Here’s what that means:

With a properly structured whole life policy, your capital is stored safely, growing with guarantees — and available when you need it.

Need to fund a project, pay for an emergency, or take advantage of an opportunity? Borrow against your policy and keep your system intact.

No sleepless nights over economic headlines. Your system keeps compounding — calmly and consistently.

Infinite Banking isn’t just a financial tool — it’s a mindset shift. It teaches stewardship, patience, and long-term thinking — the same values we celebrate every Thanksgiving.

“When you control the banking function in your life, you win.”

Control brings peace.

Peace makes space for gratitude.

And gratitude shifts your entire financial experience.

Gratitude isn’t just a feeling — it’s a responsibility.

When you take control of your financial life, you’re not only blessing yourself…

You’re creating a legacy of clarity and confidence for your family, too.

So this season, give thanks for what you have.

Then take the next step toward building something even better.

🔘 Download the Free Guide to Infinite Banking

🔘 Schedule a Call to learn how this strategy can bring peace and purpose to your money

This November, be thankful — and be intentional.

Take control.

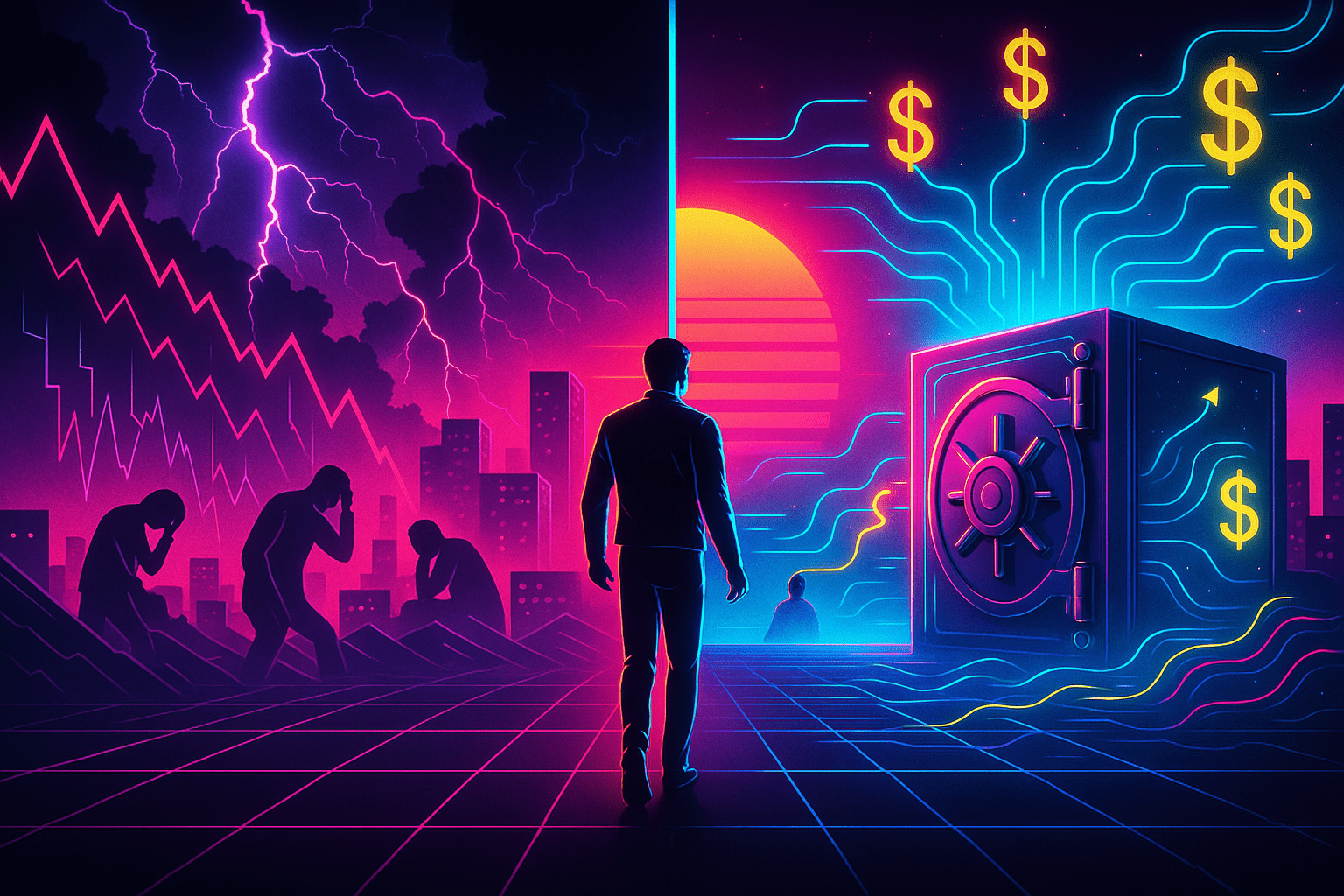

👻 It’s spooky season — but the scariest thing for most people isn’t ghosts or goblins.

It’s money.

Fear of inflation.

Fear of interest rates.

Fear of losing it all in the stock market.

Fear of not having enough.

But here’s the thing:

Fear thrives in uncertainty.

And the traditional financial system is full of it.

What if you could step out of that system — and into one built on clarity, control, and calm?

That’s what Infinite Banking offers.

Most people were never taught how money actually works.

Instead, they were taught to:

That’s a recipe for anxiety.

No wonder financial fear is so common.

The Infinite Banking Concept, developed by R. Nelson Nash, is all about creating a personal banking system using a properly structured whole life insurance policy.

Here’s how it helps replace fear with confidence:

No more wondering if your portfolio is up or down this week.

No early withdrawal penalties, no lock-up periods.

By borrowing against your cash value instead of withdrawing, your system keeps compounding in the background.

You become the banker — and set your own terms.

This isn’t a “get rich quick” trick.

It’s a process that creates predictable, long-term control over your financial future.

“The Infinite Banking Concept is a peaceful, stress-free way of life.”

When you control the banking function in your own life, the panic disappears.

You don’t have to hope. You don’t have to guess. You just follow the system.

Most people fear emergencies because they don’t have access to cash.

With Infinite Banking, you build a system where you do — and when something comes up, you can borrow against your policy, handle the need, and repay yourself on your schedule.

No begging for a loan.

No draining a 401(k).

No credit card roulette.

That’s not just financial security — it’s peace of mind.

You don’t have to live at the mercy of markets, media, or megabanks.

When you use Infinite Banking, you build a system that:

And that… is nothing to be afraid of.

🔘 Download the Free Guide to Infinite Banking

🔘 Schedule a Call and take the next step toward clarity and control

This October, make the shift from fear to freedom.

Be your own banker — and never be spooked by money again.

🌅Legacy.

It’s not just about what you leave behind — it’s about what you build into the next generation.

When people hear “generational wealth,” they usually think of trust funds, real estate empires, or massive investment portfolios. But there’s another way to pass on wealth — and it’s more accessible than you think.

It starts with control.

It continues with strategy.

And it’s powered by the Infinite Banking Concept.

Let’s be real — you don’t pass on wealth just by handing over a bank account.

If your children or grandchildren don’t understand how money works — or how to control it — the money will disappear.

What really matters is what comes with the money:

That’s what makes Infinite Banking different.

It’s not just about accumulating money.

It’s about building a family financial system that becomes a tool — not just a gift.

A properly structured whole life insurance policy from a mutual company does more than provide a death benefit.

It becomes a living financial engine you can use now — and your heirs can use later.

Here’s how it helps you build lasting wealth:

Guaranteed cash value growth and potential dividends increase the policy’s strength the longer it’s in place — setting up the next generation with a strong foundation.

Your children or beneficiaries can take policy loans, use the death benefit, or continue the system themselves — helping them fund life events without relying on banks or lenders.

When you model the process of borrowing, repaying, and using your own money efficiently — you’re teaching your kids how to be responsible, independent, and strategic.

Imagine each generation building their own policy — and becoming the “bank” for their own children. That’s not just legacy. That’s a dynasty in motion.

“The Infinite Banking Concept is not about the life insurance. It’s about the process of banking — and how families can recapture the banking function within their own lives.”

This means your policy is more than protection.

It’s a blueprint.

Every financial decision you make either strengthens or weakens your legacy.

The beauty of Infinite Banking is that it gives you the power to:

You don’t need millions to start.

You just need the mindset and the right structure.

🔘 Download the Free Guide to Infinite Banking

🔘 Schedule a Call and learn how to make Infinite Banking part of your legacy plan.

The best time to plant a tree was 20 years ago.

The second-best time is now.

Discover How to Build Wealth Using Infinite Banking

We all know we should save money.

But where you store that money?

That decision can change everything.

At first glance, it might seem like a traditional savings account is “safe.” It’s easy. It’s familiar. But if you’re looking to grow your wealth, maintain access to your capital, and create long-term financial control, it may not be the smartest place to park your cash.

This is where the Infinite Banking Concept comes in — and why a properly structured whole life insurance policy can outperform a traditional savings account in ways most people never consider.

Let’s be honest: Savings accounts at big banks offer three things:

But that’s where the benefits end.

Worst of all, you’re not in control of how your money is leveraged. The bank is.

When you use a properly structured whole life insurance policy from a mutual company (the foundation of Infinite Banking), you unlock a system that functions like a high-performance savings vehicle — but with far more advantages:

Your cash value continues to grow even when you borrow against it — and the longer your system is in place, the more efficient and powerful it becomes.

Most people keep an “emergency fund” in a bank account.

They tap into it when something unexpected happens — then spend months trying to build it back up.

With Infinite Banking, that same habit becomes more powerful:

You’re already acting like a banker — Infinite Banking just makes you an honest one.

Both savings accounts and Infinite Banking offer safety and liquidity.

But only one offers:

And only one allows you to be your own banker — instead of handing that privilege over to someone else.

You’re already setting money aside.

You already have expenses and opportunities that come up.

The question is:

Do you want your cash flow to enrich a bank?

Or do you want to build your own financial ecosystem?

That’s the power of Infinite Banking.

🔘 Download the Free Guide to Infinite Banking

🔘 Schedule a Call to walk through the numbers and get your questions answered

Let’s make your money work for you — not the bank.

As we celebrate Independence Day, it’s a good time to think about freedom—not just political freedom, but financial freedom.

According to Becoming Your Own Banker by R. Nelson Nash, one of the most powerful and overlooked opportunities in your financial life is hiding in plain sight.

It’s not about investing.

It’s not about earning more income.

It’s about how you finance the things you already buy—and who profits from those transactions.

Here’s the reality: whether you pay cash or take out a loan, you’re financing everything you buy.

If you use cash, you’re giving up the ability to earn interest on that money.

If you borrow, you’re paying interest to someone else.

In both cases… you lose.

But what if there were a third option?

Nelson Nash teaches that the most profitable thing you can finance is your own debt — because most people are already paying interest to someone else for the majority of their lives.

Think about it:

These are all expenses that flow away from you and into someone else’s banking system.

When you implement the Infinite Banking Concept using a properly structured whole life insurance policy, you create your own personal financing system.

You can:

You don’t avoid interest…

You just change who earns it.

Let’s say you typically finance a car every 5 years at 6% interest. Over your lifetime, that adds up to hundreds of thousands in payments to a bank.

Now imagine building your own policy early on.

When it’s time for your next vehicle, you borrow against your policy, make the purchase, and repay your system (on your terms). The cash value continues to grow, and the interest is redirected within your financial world—not someone else’s.

This is how wealth is quietly built over time—without chasing risky investments or hoping the market cooperates.

You’ve likely been taught to focus on investing.

But investing without control is gambling.

Infinite Banking puts you in the driver’s seat by addressing the biggest leak in most households: interest lost to outside institutions.

If you’re already financing major areas of your life, why not build a system where that money flows back to you?

That’s what Nelson Nash meant when he said:

“You finance everything you buy. You either pay interest to someone else, or you give up interest you could have earned.”

And now that you know, you get to choose.

🔘 Download the Free Guide to Infinite Banking

🔘 Schedule a Call and let’s walk through how this applies to your life

This Independence Day, start your journey toward real financial freedom — by becoming your own banker.

🕶️We’re six months into the year.

Some people are on track.

Others are behind.

And some are realizing they never actually set clear financial goals in the first place.

Wherever you’re at — there’s still time.

This isn’t about catching up. It’s about leveling up.

And with the right strategy, the second half of the year can become the launchpad for lasting momentum.

Let’s be real:

Most people either…

But there’s a better way.

The truth is, you don’t need a miracle or a market rally to make progress.

You need a system — one that puts you in control.

This is where the Infinite Banking Concept comes in.

Instead of relying on banks, credit cards, or unpredictable investment accounts, you can build your own personal banking system using a properly structured whole life insurance policy.

When designed the right way, this policy allows you to:

It’s not magic.

It’s a system. And it gets stronger the longer you use it.

Here’s the cool part:

When you implement Infinite Banking now, you’re not just finishing the year strong —

you’re setting up every year after that to work even better.

This isn’t just a one-time fix.

It’s a foundational shift that helps you:

Don’t let the halfway point make you feel behind.

Let it remind you: you still have time to take charge.

Whether your goal is to improve cash flow, get rid of debt, save for something big, or build long-term wealth — Infinite Banking gives you the tools to do it.

And the best time to build momentum?

🔘 Download the Free Guide to Infinite Banking

🔘 Schedule a Call to explore your options

You don’t need another year of hoping it’ll all work out.

You need a strategy that puts you back in the driver’s seat.

| UPDATE! DUE TO UNFORSEEN CIRCUMSTANCES, THIS EVENT HAS BEEN POSTPONED. |

Discover the powerful strategy families in Ken-Caryl area are using to take back control of their money — without relying on Wall Street or big banks.

| What You’ll Learn |

| 📈 How to grow wealth without risking it in the market | 💸 How to access your money without taxes or penalties |

| 🎓 A smarter way to plan for college, retirement, emergency savings & more | 🏛 How controling the banking function in your life can benefit families for generations |

This isn’t about getting rich overnight — it’s about peace of mind, flexibility, and legacy.

Most families do the “right” things — they save, invest, and hope the market holds up. But with rising inflation, tax uncertainty, and the cost of living going up every year… the old way isn’t working like it used to.

That’s why families in Ken-Caryl are rethinking their financial game plan — not just for retirement, but for all of life’s big expenses.

Imagine having a strategy that lets you:

It’s not wishful thinking. It’s a 100-year-old strategy that’s still being used by some of the most financially savvy families — The Infinite Banking Concept. But here’s the truth: you don’t have to be wealthy to use it.

This strategy is designed for everyday people who want more control, flexibility, and peace of mind. It works whether you’re just starting to build your financial foundation or already planning for retirement. You just need to understand how it works — and that’s exactly what this event is for.

📅 Thursday, June 19, 2025

🕕 6:30 – 8:00 PM (Doors open at 6:15 for refreshments)

📍 Ken Caryl Ranch House – Bradford Room (7676 S. Continental Divide Road)

🥤 Light snacks & beverages provided

💺 Limited Seating – RSVP Preferred

*

Hi, I’m Jason — and I live right here in Ken-Caryl area, just like you.

For years, I’ve helped families and business owners rethink the way they handle their money — not through risky investments, but through time-tested strategies that prioritize control, stability, and long-term growth.

After seeing so many of my neighbors feeling unsure about retirement, college costs, or just how to keep up financially, I decided it was time to host something local — something real.

This event is designed to give you clarity, confidence, and a fresh perspective on how your money can work for you.

Register

| UPDATE! DUE TO UNFORSEEN CIRCUMSTANCES, THIS EVENT HAS BEEN POSTPONED. |

🎓 Most people spend the first 20 years of their life learning how to make a living—but not how to build wealth. You might have studied algebra, Shakespeare, or U.S. history… but chances are, no one taught you how money really works.

That’s not an accident.

And that’s why so many hardworking people still feel like they’re spinning their wheels—earning income, paying bills, and watching wealth slip through their fingers.

Let’s change that. Starting now.

From student loans to credit cards to 401(k)s, most traditional financial advice teaches you one thing: hand control of your money over to someone else.

You’ve been taught to save what’s left after spending.

You’ve been taught to “hope it all works out in the long run.”

But real wealth builders? They flip that model upside down.

Wealth isn’t just about income.

It’s about what you keep, what you control, and how your dollars work for you.

This is where the Infinite Banking Concept comes in.

By using a properly structured whole life insurance policy, you create a system that gives you:

This isn’t theory.

It’s a time-tested strategy that many wealthy families and entrepreneurs have used for generations—quietly.

The good news?

You don’t need a finance degree, a Wall Street broker, or a six-figure income to start building wealth the smart way.

You just need to:

The earlier you start, the more powerful it becomes—but the key is starting.

Even a small policy, used the right way, can create long-term momentum.

You’re not behind. You’re just stepping into the real classroom now.

And this time, the lesson is clear:

Take back control of your money, and you take back control of your future.

🔘 Download the Free Guide to Infinite Banking

🔘 Schedule a Call to see how this strategy could work for you

Let’s rewrite your financial future—starting now.

Spring cleaning isn’t just for closets and garages. It’s also a powerful time to reevaluate how you handle money — what’s working, what’s not, and what habits are quietly draining your financial potential.

Here are three outdated money habits worth tossing out — and smarter alternatives to take their place.

The Habit:

Leaving your savings in a traditional bank account “just in case.”

The Problem:

Your money sits still. You’re earning next to nothing in interest, and with inflation rising, your dollars are quietly losing purchasing power every year. That’s not to say you shouldn’t have some money stored away in this fashion. You should! But perhaps just enough to get you through immediate emergencies, today.

The Shift:

Start warehousing your wealth in a system that grows and works for you — even while you use it.

The Infinite Banking Concept uses a properly structured whole life insurance policy as a powerful financial engine:

Your dollars shouldn’t collect dust. They should multiply.

The Habit:

Relying on credit cards, lines of credit, or personal loans to handle unexpected expenses or to finance big goals.

The Problem:

You’re paying interest to someone else — which means your future earnings are already spoken for.

The Shift:

Build your own personal financing system.

When you implement the Infinite Banking Concept, you create access to capital you own and control, allowing you to finance life’s needs — on your terms. You pay yourself back, not a lender.

It’s about changing the flow of money so it stays within your ecosystem.

The Habit:

Putting off financial strategies until the timing feels perfect, or income feels “high enough.”

The Problem:

Time is your most valuable asset — and the longer you wait, the harder it becomes to build long-term momentum.

The Shift:

Start with what you can now.

Many people begin their Infinite Banking journey with modest monthly premiums and scale up over time. It’s not about perfection — it’s about direction. Even a small system, started today, can grow into something powerful over time.

Spring is a season of fresh starts — and your finances are no exception.

By ditching old habits and building new ones through the Infinite Banking Concept, you’re not just cleaning house — you’re setting the foundation for a smarter, more sustainable financial future.

🔘 Download the Free Guide to Infinite Banking

🔘 Schedule a Call to Talk Strategy

Let’s clean out the financial clutter and build something that lasts.

The Current Lending Environment is Squeezing Investors

Real estate investors have always needed access to capital, but 2024 and beyond is proving to be a particularly difficult landscape. Banks are tightening their grip on credit, making it harder for investors to secure financing for both new property acquisitions and refinancing existing projects.

According to the Federal Reserve’s August 2024 Senior Loan Officer Opinion Survey, banks continued to tighten lending standards across all commercial real estate (CRE) loan categories. Loan-to-value ratios are being reduced, debt-service coverage requirements are increasing, and banks are scrutinizing borrower liquidity and reserves more than ever.

This tightening is not just a U.S. problem. In January 2025, the European Central Bank reported that banks across the eurozone had restricted credit access for companies during Q4 2024, with further restrictions expected. The global ripple effect is clear: lenders are nervous, and investors are feeling the squeeze.

How Does This Impact Real Estate Investors?

When banks pull back, it can cause ripple effects across an investor’s entire portfolio.

The Infinite Banking Concept as a Strategic Solution

This is where the Infinite Banking Concept (IBC) becomes invaluable for real estate investors.

IBC involves using a specially designed, dividend-paying whole life insurance policy from a mutual insurance company. Over time, this policy accumulates cash value, which can be borrowed against through policy loans.

The key benefits of IBC for investors, especially in today’s lending environment, are:

Real-World Applications: An Investor’s Advantage

There are countless ways savvy real estate investors can leverage the cash value from their policies to fund their deals and manage their portfolios. Here are some high-level applications:

These flexible uses of cash value empower investors to control their deals and seize opportunities on their own terms—without waiting on a bank’s approval or risking a good deal slipping away.

Why This Approach Matters More in 2025

Let’s face it—we are living in a time of economic uncertainty. The U.S. national debt is over $34 trillion, and interest rates are holding at their highest levels in decades. This kind of environment is precisely why real estate investors need financial independence from traditional banks. You need the ability to act quickly and decisively.

The Psychological Shift: Becoming Your Own Banker

The Infinite Banking Concept is not just about life insurance or policy loans. It is about changing how you think about financing. Instead of being at the mercy of banks, you gradually build your own source of capital.

Each deal funded through your policy loan is another step toward financial autonomy. You shift from being a borrower dependent on bank policies to a decision-maker using your own financial system.

Policy Growth Is Not Stopped by Loans

One of the most misunderstood aspects of IBC is how the cash value continues to grow, even when you take out a policy loan. Your cash value is not being spent; you are borrowing against it, using the insurance company’s funds as collateral.

This means your policy earns dividends and grows on the full cash value, regardless of any outstanding loans. The loan itself is repaid on your terms, often using rental income or profits from property flips.

Tax Efficiency and Protection

In addition to offering liquidity, IBC policies come with tax advantages:

Comparing IBC to Traditional Financing

Let’s break it down:

| Factor | Traditional Bank Financing | Infinite Banking (Policy Loan) |

| Approval Process | Lengthy, credit-based | Quick, policy-based |

| Access Speed | Weeks | Days |

| Loan Terms | Bank-controlled | Investor-controlled |

| Repayment Schedule | Fixed | Flexible |

| Growth During Use | None | Policy cash value grows |

| Tax Benefits | Limited | Significant |

The Bottom Line

In 2025, real estate investors cannot afford to be handcuffed by bank lending policies. The Infinite Banking Concept provides a practical, proven way to unlock capital on your terms. It offers more than just an alternative financing tool—it represents a shift toward financial autonomy.

As the lending landscape tightens, those who embrace IBC will find themselves positioned to seize more opportunities, close deals faster, and ultimately build lasting wealth.

If you want to learn more about implementing IBC as part of your real estate investing strategy, visit 1024Wealth.com/realestate and discover how to finance on your terms.

Download the free e-book, A Real Estate Investors Guide to Infinite Banking, at 1024Wealth.com/realestate.

Jason K Powers is a Multi-Business Owner, Real Estate Investor and an Authorized IBC Practitioner. In an exclusive partnership with the National Real Estate Investor Association, Jason is the go-to expert for all aspects of Infinite Banking and Life Insurance. Connect with Jason today to explore how life insurance can empower you to reach your financial goals.

In the world of real estate investing, the importance of managing your cash flow and maintaining control over your financial resources cannot be overstated. Yet, many investors find themselves with wealth tied up in traditional investments and qualified retirement plans that often carry significant risks. These traditional vehicles are frequently exposed to market volatility, leaving your hard-earned money vulnerable to fluctuations beyond your control. Additionally, the lack of liquidity in these investments can pose a problem; accessing your funds, especially from qualified retirement plans, can lead to penalties and taxes, eroding the value of your wealth. While some investors may be comfortable with these risks, understanding and owning them as part of their overall strategy, the question remains: Is there a better way to safeguard your wealth while maintaining control and flexibility

Imagine a strategy that allows you to maintain full control over your money, ensures consistent growth, and provides penalty-free access whenever you need it. This approach isn’t bound by the constraints of traditional financial systems. Instead, it empowers you to become your own banker, giving you the flexibility to use your capital when opportunities arise without interrupting its growth. Imagine having the ability to fund a new real estate investment, cover unexpected expenses, or take advantage of a lucrative deal, all while your wealth continues to grow uninterrupted.

Enter the Infinite Banking Concept, a strategy coined by R. Nelson Nash, which revolutionizes the way you think about and manage your finances. The core purpose of Infinite Banking is to regain control of the banking function in your life. By becoming your own banker, in effect, you can take advantage of uninterrupted compounding of your wealth, while still having the ability to access and utilize your funds whenever you need them. Unlike traditional banking systems, where you are dependent on external lenders and financial institutions, Infinite Banking puts you in the driver’s seat, allowing you to leverage your capital to your advantage. This is not just about creating a financial strategy—it’s about creating a financial system that works for you, providing stability, flexibility, and growth throughout your entire life.

Imagine if you could access your wealth whenever you needed it, without the fear of penalties or market downturns affecting your plans. Imagine using your funds to seize a once-in-a-lifetime investment opportunity, knowing that even while you’re using the money, it’s still growing in the background. Picture a financial future where you are not only securing your retirement but doing so on your terms, with a stable and reliable source of income that you’ve built over time. By controlling the banking function in your life, you can create a legacy of financial freedom that extends beyond your working years, ensuring that your wealth continues to serve you and your loved ones for generations to come.

In essence, this strategy is about taking control of your financial future and using your resources in the most efficient and effective way possible. The Infinite Banking Concept allows you to navigate the complexities of real estate investing with confidence, knowing that your wealth is growing steadily, and you have the flexibility to access it when you need it.

—————————–

Jason K Powers is a Multi-Business Owner, Real Estate Investor and an Authorized IBC Practitioner. In an exclusive partnership with the National Real Estate Investor Association, Jason is the go-to expert for all aspects of Infinite Banking and Life Insurance. Connect with Jason today to explore how the Infinite Banking Concept can empower you to reach your financial goals.

The world of real estate investing, where capital flow dictates growth and success, often puts investors at the mercy of banks, hard money lenders, and private money lenders. These financing avenues, although reliable, come with their unique set of drawbacks. Enter R. Nelson Nash’s concept of ‘Becoming Your Own Banker’, a revolutionary paradigm detailing the ‘Infinite Banking Concept’. For real estate investors, it’s essential to analyze how this strategy might be more advantageous than traditional financing channels.

Traditional Financing vs. Infinite Banking

Most real estate investors are familiar with the process: find a profitable property, negotiate the price, and then hunt for a lender. Traditional lenders, including banks and hard money lenders, charge interests which can sometimes be exorbitant, especially in a volatile market. Moreover, there are approval processes, credit checks, and at times, hidden fees that can eat into the profit margins.

On the other hand, Nash’s Infinite Banking Concept advocates for individuals to leverage their whole life insurance policies. In essence, it’s about utilizing a properly structured policy, borrowing against its cash value, and then repaying it at one’s convenience. In this model, you’re both the borrower and the lender. You control the repayment schedule and, more importantly, you’re recapturing your principle amount time and time again. The key difference here lies in the control and flexibility it offers over traditional methods.

The Numbers Game

To illuminate this concept, let’s delve into a hypothetical scenario using $100,000 with both the bank and your own properly structured policy. To simply the example, we’ve annualized the amounts, so you can see what’s happening on a larger scale.

Borrowing from a Lender: You borrow $100,000 from a traditional lender at an interest rate of 4%. By the end of the year, you owe them $104,000 ($100,000 principal + $4,000 interest).

Costs & Growth: While you owe the bank $4,000 in interest, there’s no growth on your principal. The full cost of borrowing is $4,000.

Borrowing from Your Policy with Dividend-Driven Growth: You have built up a cash value of $100,000 in your policy.

Growth Rate Including Dividends: The policy (principle) grows by a total of 5% that particular year due to dividends, increasing your available cash value by $5,000. By year’s end, without considering the loan, the gross cash value is $105,000.

Taking a Loan: You borrow the same $100,000 from your policy at a rate of 4%, owing $4,000 in interest at the year’s end.

Net Growth: Even after paying off the interest, you’re left with a net positive growth of $1,000.

Contrasting the Two Scenarios:

Interest Cost: With the traditional bank, you’re out $4,000. With the policy loan, after considering the dividend-driven growth, you’re ahead by $1,000. That’s a clear difference of $5,000 between the two borrowing methods.

Asset Growth: In the bank scenario, there’s zero growth on your borrowed money. You borrowed the banks money, and are giving it back to them. In contrast, your policy’s cash value grew, amplifying your assets, even as you utilized it for a loan. You will also be re-capturing that principle balance to be used on something else, without having to apply for another loan and go through the rigorous process again and again.

Flexibility & Control: With the traditional bank loan, you’re bound by their repayment terms and conditions, which might include penalties for early repayment or other unforeseen charges. Borrowing against your policy offers more flexibility, allowing you to control the repayment terms and other dynamics.

Privacy & Credit: While traditional banks will go through a vetting process, including credit checks, borrowing from your policy remains a private transaction. More importantly, taking a loan against your policy doesn’t affect your credit score. This means your borrowing capacity remains undiminished in the eyes of the credit world, allowing you to maintain a strong financial position for other investments or necessities that require a favorable credit score.

Conclusion:

When evaluating the two scenarios, it becomes evident that borrowing from your properly structured, dividend-paying whole life insurance policy is not just about low-interest rates. It’s about holistic financial growth, maintaining control over your assets, and reaping the benefits of compounded growth. Even when the loan interest rates mirror each other, as in this example, the intrinsic growth and compounded benefits of a life insurance policy make it a more advantageous avenue for astute real estate investors.

For real estate investors, the goal has always been to maximize ROI while minimizing costs. Traditional financing avenues, with their rigid structures, have been the conventional route. But as the industry evolves, it’s prudent for investors to seek out novel, efficient strategies for financing. Nash’s ‘Infinite Banking Concept’, applied wisely, could be the gateway to enhanced financial freedom and success in the real estate domain.

—–Jason K Powers is a Multi-Business Owner, Real Estate Investor and an Authorized IBC Practitioner. In an exclusive partnership with the National Real Estate Investor Association, Jason is the go-to expert for all aspects of Infinite Banking and Life Insurance. Jason works with clients across the country showing them how to achieve their financial goals by taking control of the banking function in their life and creating financial velocity that can last for generations. Connect with Jason today to explore how the Infinite Banking Concept can empower you to reach your financial goals.

As real estate investors, we’re all too familiar with the challenges of securing capital. From navigating the ever-changing terms of lenders to facing exorbitant interest rates, the obstacles can feel endless. Add to that the frustration of opportunity costs—the returns we miss out on because our money is tied up in someone else’s system—and it’s clear that the traditional financial system often works against us.

Relying on banks and other lenders leaves us at their mercy. Approval processes are slow, repayment terms are rigid, and profits shrink as interest payments eat into our bottom line. This dependency restricts our growth and flexibility, keeping us locked in a cycle that feels impossible to escape. But it doesn’t have to be this way.

What if you could fund your own deals on your terms?

Imagine having access to capital whenever you need it—without waiting weeks for approval or worrying about a lender’s agenda. And think about the freedom that comes with building a financial system that works for you, not against you. As real estate investors, our ultimate goal is financial freedom—a life where our investments generate predictable, uninterrupted growth.

This is where the Infinite Banking Concept (IBC) comes in. It’s not a product; it’s a process—a way to “be your own banker.” With IBC, you create your own private financial system, enabling you to recycle and reuse your capital. Instead of depending on external lenders, you become the banker, controlling your cash flow, funding your investments, and creating a legacy of wealth that grows predictably over time.

The philosophy behind Infinite Banking is simple but powerful. It requires us to shift how we think about money—not just as something we earn and spend, but as a tool that can continuously grow and work for us. By building a system of uninterrupted, compounding growth, we gain independence from banks and lenders while maintaining liquidity and control.

Here’s how the process works.

You build a financial reservoir—a private pool of capital that becomes your go-to source for funding deals, covering expenses, or seizing opportunities. When you borrow from this reservoir, you’re borrowing from yourself, not an external lender. As you repay it, your system continues to grow, creating a cycle of wealth that strengthens with each use.

For real estate investors, the benefits are transformative. Imagine having instant access to funds for your next deal, financing projects on your terms, and repaying yourself instead of a bank. With IBC, your money works harder and stays within your control. Plus, your financial system grows predictably, immune to market volatility or lender restrictions.

Let’s bring it to life with an example. Suppose you find a property that fits your portfolio perfectly, but you need $100,000 to close the deal. With IBC, you borrow against your reservoir, securing the property quickly and without interference. As the property generates rental income or appreciates in value, you repay yourself on your schedule. Meanwhile, your reservoir has continued to grow, uninterrupted, ensuring you’re ready for the next opportunity.

This is the essence of Infinite Banking: breaking free from financial dependency.

It empowers you to take control of your financial future, eliminate the stress of dealing with lenders, and build a system that supports your goals and dreams.

If you’re ready to move beyond the constraints of traditional financing, Infinite Banking can help you get there. To learn more about this process and how it can transform your real estate investing journey, visit www.1024wealth.com/NREIA and take the first step toward financial freedom.

—Jason K Powers is a Multi-Business Owner, Real Estate Investor and an Authorized IBC Practitioner. In an exclusive partnership with the National Real Estate Investor Association, Jason is the go-to expert for all aspects of Infinite Banking and Life Insurance. Connect with Jason today to explore how life insurance can empower you to reach your financial goals.

To understand the unique approach of the Infinite Banking Concept (IBC), it’s essential to first delve into the foundational practices of the modern U.S. banking system – particularly, fractional reserve banking. This system, where banks are required to keep only a fraction of their total deposits in reserve and are free to lend out the remainder, is a cornerstone of contemporary finance. While the theory is that it fosters economic growth through increased lending (and most certainly enables banks to generate significant profits), it also introduces significant risks such as bank runs, asset bubbles and destabilization of the financial system at large, as we’ve seen time and time again.

Fractional reserve banking effectively creates money out of thin air. For every dollar deposited, only a fraction is kept on hand, and the rest can be used for loans. Before 1992, banks were required to keep 12% of deposited amounts on reserve. This meant they could loan out the remaining 88%. In 1992, that reserve was lowered to 10%. This now meant that 90% could be loaned out. In March of 2020, following the shockwave of COVID-19, the Federal Reserve lowered that requirement to an unprecedented 0% (Zero Percent), where it has remained to date. We all know what this means.

This can lead to a multiplicative effect in money supply creation, potentially leading to inflation if not carefully managed. Through the lens of Austrian Economic theory, we would argue that it leads to unsustainable credit expansion that can cause economic bubbles and crashes. Austrian economists advocate for a banking system based on sound money principles – where money supply expansion is tightly controlled and closely tied to real assets like gold, thereby promoting economic stability and reducing inflation risks.

Transitioning to Infinite Banking Concept

Against the backdrop of these potential instabilities inherent in fractional reserve banking, R. Nelson Nash introduced the Infinite Banking Concept. Nash proposed that individuals could become their own bankers, thus sidestepping some of the systemic risks posed by traditional banking practices. By utilizing dividend-paying whole life insurance policies as financial tools, individuals can build a personal banking system. This system allows policyholders to borrow against the cash values of their policies rather than depending on commercial banks for loans.

Here’s how it works: a policyholder pays into a properly structured whole life insurance policy designed specifically for the purposes of Infinite Banking, which over time accumulates a cash value. This cash value grows at a guaranteed rate and also earns dividends. Policyholders can then borrow against this cash value for personal (or business) financing needs – whether for buying a car, investing in real estate, or funding a child’s education – without having to go through a traditional bank. Now you, the policy holder, is in control of the banking function in your life. Imagine a life without the bank.

The beauty of this system lies in its simplicity and control. Loans taken against a life insurance policy come with no mandatory repayment schedule, and the interest rates are typically lower than those of bank loans. Moreover, since the policyholder is borrowing against their own savings, they are essentially paying themselves back, thus keeping the money within their personal economy.

Infinite Banking as a Sound Money Solution

From an Austrian Economic perspective, the Infinite Banking Concept resonates strongly with the theory’s core principles. Austrian Economics favors systems that minimize the risk of inflation and promote fiscal conservatism. By encouraging individuals to save and build their wealth within a life insurance policy – a historically stable and non-volatile asset – IBC promotes financial self-reliance and stability.

Moreover, by reducing reliance on traditional banks and their loan products, individuals using the Infinite Banking Concept mitigate the risk of being adversely affected by broader economic downturns or banking crises. They create a buffer against economic uncertainty by leveraging their life insurance policies to fund their borrowing needs.

In conclusion, while fractional reserve banking has facilitated economic expansion and prosperity on a massive scale, it is not without significant risks – risks that are amplified by the very nature of the banking practice as critiqued by Austrian Economics. The Infinite Banking Concept offers a compelling alternative that not only aligns with Austrian principles of sound money but also empowers individuals by making them their own financial managers. By building wealth in a controlled, self-sustained banking system, individuals can achieve greater financial security and independence, making the Infinite Banking Concept a prudent choice in an uncertain economic landscape.

—Jason K Powers is a Multi-Business Owner, Real Estate Investor and an Authorized IBC Practitioner. In an exclusive partnership with the National Real Estate Investor Association, Jason is the go-to expert for all aspects of Infinite Banking and Life Insurance. Connect with Jason today to explore how life insurance can empower you to reach your financial goals.

The Recent Banking Crisis

The recent banking crisis, marked by the collapse of several major financial institutions, has been a wake-up call for investors worldwide. This crisis has unveiled a hard truth: the traditional banking system, often perceived as a bedrock of financial stability, can be incredibly fragile. Banks, even those with longstanding reputations and seemingly robust structures, have been unable to withstand the economic pressures, leading to sudden collapses. These failures have left countless customers in the lurch, struggling to regain control of their financial futures.

For real estate investors, this crisis has posed significant challenges. The property market, inextricably linked with the financial sector, has felt the shockwaves of these banking collapses. Investors have had to grapple with issues such as frozen assets, interrupted cash flows, and declining property values, and even not being able to get checks written or cashed, casting shadows of uncertainty over their investments.

In such a volatile environment, the question arises: is it prudent for investors to continue trusting all of their hard-earned money to these unstable institutions?

Or is there a safer, more reliable alternative?

Enter the Infinite Banking Concept (IBC)…

This financial strategy, grounded in the principles of self-reliance and financial autonomy, empowers you to become your own banker. Instead of depositing money into traditional banks that may falter or fail, IBC encourages individuals to utilize properly structured whole life insurance policies with cash values. These cash values can be borrowed against, ensuring that your money remains within your control, and providing a safety net in the face of banking crises. With IBC, your financial security is no longer at the mercy of external institutions, but rests firmly in your own hands.

The U.S. Inflation Crisis and Infinite Banking Concept as a Hedge

The U.S. is also currently grappling with a significant inflation crisis, the likes of which haven’t been seen in decades. Consumer prices are soaring, the cost of living is on the rise, and the dollar’s purchasing power is rapidly eroding. This economic climate can be particularly detrimental for real estate investors. As inflation increases, the real value of rental income can decrease, and the cost of property maintenance can escalate, both factors potentially eating into your profit margins.

Furthermore, inflation can also affect the value of money sitting in traditional banking accounts. When inflation rates surpass the interest rates offered by these accounts, the real value of your savings diminishes over time. In essence, your money is losing value while it sits idle in the bank.

This inflation crisis underscores the need for a solid, reliable hedge—a way to protect and potentially grow your wealth despite escalating prices. Here, the Infinite Banking Concept (IBC) presents a compelling solution. The cash values in properly structured whole life insurance policies, the cornerstone of IBC, grow on a tax-advantaged basis. These policies provide a guaranteed, contractually ensured rate of return that often outpaces inflation rates due to its compounding nature. Unlike traditional banking, the value of your ‘bank’ under the IBC is not directly tied to the economy’s performance. This financial insulation offers a level of protection against inflation, helping to preserve your purchasing power and safeguard your wealth.

The Infinite Banking Concept in Real Estate Investment

The beauty of the Infinite Banking Concept (IBC) is its universality. This strategic financial approach isn’t the exclusive domain of the wealthy or financially elite—it’s accessible and beneficial to anyone, regardless of their current financial standing or investment portfolio size.

In the realm of real estate investment, many potential investors are daunted by the significant capital often required to enter the market. Properties, especially in popular or high-demand areas, can carry hefty price tags. Add to that the potential costs of renovation, maintenance, and property management, and it can feel like a financial mountain too steep to climb.

However, the IBC presents a potential solution to this hurdle. When you adopt the Infinite Banking Concept, you are essentially establishing a personal banking system. This properly structured whole life insurance policy accumulates a cash value over time, against which you can borrow to fund your investments. This mechanism allows you to tap into a source of capital that grows over time and remains under your control.

So, whether you’re a seasoned real estate investor looking to expand your portfolio or a newcomer eager to make your first property purchase, the Infinite Banking Concept can provide the financial foundation and flexibility you need. It is a strategy that transforms the intimidating financial mountain into a manageable, even scalable, hill throughout one’s lifetime.

Moreover, the death benefit associated with the insurance policy provides a financial safety net for your loved ones, adding an extra layer of security to your investments. And as your policy’s cash value grows over time, so does your ability to invest and generate wealth.

Conclusion

In today’s uncertain economic environment, the Infinite Banking Concept can provide real estate investors with a stable and secure financial strategy. It offers protection against banking crises and hedges against inflation, all while providing a powerful tool for real estate investment. Regardless of your financial status, the Infinite Banking Concept is an accessible and practical tool to harness.

Not only does it safeguard your wealth, but it also provides a continuous flow of capital for your real estate investments. By leveraging the IBC, you’re not just saving for the future; you’re actively investing in it.

The banking crisis and inflation serve as reminders of the inherent risks in traditional financial systems. By contrast, the IBC allows you to take control of your finances, mitigating risk and promoting growth. For real estate investors, it is a pathway to greater financial freedom and security.

In a world of financial uncertainty, the Infinite Banking Concept is more than just a strategy—it’s a revolution in personal finance that empowers each individual to become their own bank. It is time to explore this opportunity and witness the potential it holds for your real estate investment journey.

—Jason K Powers is a Multi-Business Owner, Real Estate Investor and an Authorized IBC Practitioner. In an exclusive partnership with the National Real Estate Investor Association, Jason is the go-to expert for all aspects of Infinite Banking and Life Insurance. Connect with Jason today to explore how life insurance can empower you to reach your financial goals.

~ Let no man seek the good of his own, but that of his neighbor. 1 Corinthians 10:24 ~